Quick Facts About the Car Buying and Selling Marketplace

The summer of 2024 is an odd time to be car shopping. We have good news, bad news, and disruptive news for those of you in the market. But, when you’ve read it all, the lesson will be a timeless one — do your homework and take your time. There is no reason to rush a big financial decision.

The good news: prices for new and used cars have been in a slow, steady decline most of the year. The bad news: interest rates remain high, and won’t drop this summer. It’s harder than normal to qualify for a loan right now. And, when you do qualify, your payments will be higher thanks to the interest rate.

The disruptive news: a major cyberattack in June slowed and scrambled business at many car dealerships. Their operations are back to normal now, but it will take weeks for their inventory and record-keeping to catch up. That may complicate finding the car you want this month. Car dealerships use industry-specific software, called a Dealership Management System (DMS), to manage everything from tracking inventory to scheduling service appointments to paying employees. The June cyberattack took one of the largest DMS providers offline for almost two weeks.

Dealerships reverted to slower pen-and-paper processes to complete sales. Now that the computer system works again, they’re trying to update records of all those sales during their downtime between new sales. It will take time for dealers to know precisely what vehicles they still have in stock.

Dealers typically mark down prices when they’re overstocked. However, some don’t yet have up-to-date records they can rely on to make those decisions. That situation improves by the day. But it can make finding the exact combination of colors and features you want challenging this month.

We’ll walk you through what to expect while buying or selling a new or used car or trading one in. Many car shoppers are in both markets simultaneously, with a vehicle to swap. They’re likely to find balanced offers on their trade-in this month. Read on to find out more.

What New Car Shoppers Can Expect

Simple supply and demand governs car prices in America. When dealers are oversupplied, they mark vehicles down to attract business. When they’re undersupplied, they can charge more than the manufacturer’s suggested retail price (MSRP) and trust that buyers will still be interested.

Traditionally, they aim to keep about 60 days’ worth of new cars in stock. An old industry rule of thumb tells them that’s the sweet spot. When dealers have about as many cars on the lot as they can sell in 60 days, they typically have something on the lot that appeals to most shoppers. Using that guide keeps dealers from overspending on inventory that isn’t selling.

Before the cyberattack, the average dealership had about 74 days in stock. However, the attack disrupted recordkeeping, making it hard to get an accurate estimate for July.

New vehicle prices have mostly held steady despite the chaos. The average new car buyer in June paid $48,644 — just $266 more than in May and $307 lower than in June 2023. Discounts made up 6.4% of the average sale.

Those numbers are likely to hold fairly steady in July. However, what you can expect changes based on which car you’re considering. Toyota, Lexus, and Honda remain undersupplied and sell most vehicles for close to MSRP.

Stellantis, parent company of brands including Alfa Romeo, Chrysler, Dodge, Fiat, Jeep, and Ram, has had about twice as much inventory as it should for much of the year. Those dealers have been discounting aggressively.

But don’t be surprised to find that a car listed on a dealer’s website is not actually available this month. Dealers may be recovering from the hack well into late summer.

RELATED: When Will New Car Prices Drop?

Two other factors are increasing the cost of a new car right now. Car insurance costs and car loans.

While new vehicle prices are coming down, car insurance premiums spiked. Car insurance prices have grown so high in the last year that we now encourage shoppers to get insurance quotes on any car they’re considering before they put a dollar down. Insurance costs might make you consider a different vehicle.

The other is that while it’s easy to find a decent deal on a good car this month, it’s much harder to find a good car loan.

Interest Rates May Fall Later This Year

The cost of a new vehicle is fairly reasonable this month, but the borrowing costs to buy one are not.

The Federal Reserve, commonly called the “Fed,” sets the interest rate banks use when they lend each other money. That Fed rate governs rates for every other kind of loan, including car loans. The Fed raised rates last year to combat inflation but said it expected to cut them this year when the trick worked. It isn’t working quickly.

So they’re keeping rates high. The Fed once said it hoped to cut rates several times early this year. It’s now predicting just one cut, no earlier than September. Since most shoppers borrow to buy a new car, the raised rate keeps the monthly cost of a new car high.

The average buyer in June signed up to spend the equivalent of 37.2 weeks of earnings on a new car. Lenders also tightened their standards, making it harder to qualify for a new car loan.

However, interest rates are limiting many shoppers’ options. Very few of us are cash buyers. Many who expect to borrow for their next car might benefit from waiting for the next rate cut.

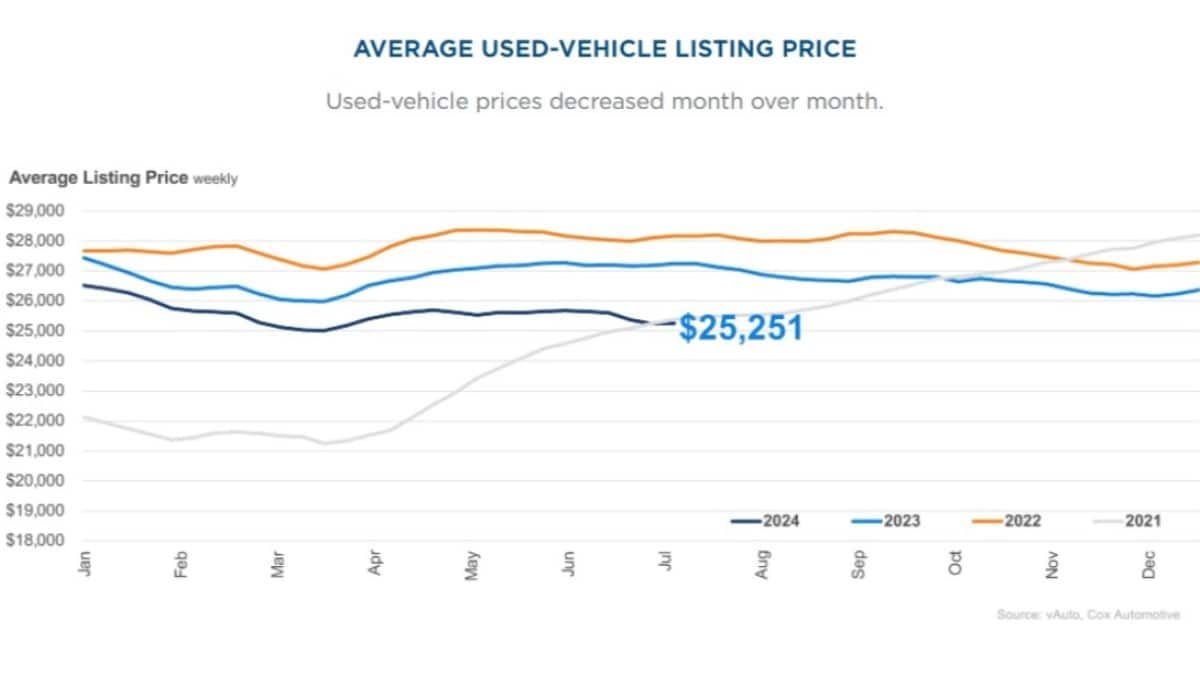

What Used Car Shoppers Can Expect

Used car prices are dropping. The average used car was listed for $25,251 in June, down about $400 from May’s price and more than $1,700 from last June.

That trend may not last — the wholesale prices dealers pay at auction for the used cars they later sell increased slightly during the month. Wholesale price changes tend to become retail price changes about six to eight weeks later, so a slight increase may come in late summer.

The cyberattack also impacted the used car side of some dealerships. Shoppers should be prepared for some dealers to have problems keeping tabs on their used car inventory this month. But that should ease by the day as dealerships catch up on inputting all the transactions they conducted while systems were down.

The nationwide used car supply will likely remain thin for years. Pandemic-era disruptions meant automakers built about 8 million fewer cars than they otherwise would have in 2021 and 2022. That’s 8 million cars that will never reach the used market, keeping supplies low for a long time.

With many buyers staying home thanks to high interest rates, dealers are still being reasonable with prices.

The only problem used car shoppers may encounter this month is a small supply of the older, higher-mileage used cars dealers sell for under $15,000. That shortage has been a constant through most of 2024, and we don’t anticipate it changing this year.

Automakers Are Building More Expensive Cars

Though short-term trends may push new car prices down, automakers are focusing efforts on building more premium cars. The era of the inexpensive car is disappearing. A recent analysis finds that sales of cars priced at $25,000 or less have fallen by 78% in just five years. Five years ago, automakers offered 36 new models in that price range. This year, that number is just 10. Meanwhile, those priced at $60,000 or higher have grown by 163% during the same period.

Cox Automotive Chief Economist Jonathan Smoke explains that last year’s Federal Reserve interest rate hikes kept some shoppers from buying cars. “This trend induces automakers to focus on profitable products for consumers who can afford to buy, which keeps less affluent consumers out of the new vehicle market altogether and limits what is available and possible in the used market for years to come,” Smoke cautions. Cox Automotive is the parent of Kelley Blue Book.

Dealers are pushing back, telling automakers they need more affordable cars to sell. But correcting the problem will take time. You’ll likely find affordable cars in short supply on many sales lots.

Older, Less Expensive Cars Harder to Find

If you hope to find an older vehicle and your budget is less than $15,000, these cars remain in short supply. More would-be new car shoppers started buying up the available used vehicles, drawing down the inventory. Plus, Americans are holding onto their cars longer than ever. The average vehicle on American roads is now 12.6 years old. Automakers also produced fewer cars for several years after the 2008 recession, leaving fewer higher-mileage, older used vehicles available to sell.

The most accessible used cars are priced between $15,000 and $30,000.

How to Buy a Car Right Now

If you want a new or used vehicle, shoppers are still getting sticker shock. New car prices remain about 13% higher than three years ago when the average transaction price for new vehicles was around $42,200. But take stock that your next car will likely last longer and help you drive safer than ever with all the technological advances and offerings.

RELATED: Buying Older, Used Cars in 2024

Vehicle quality studies repeatedly show that today’s new cars suffer fewer problems than those from just a few years earlier. Buyers of higher-priced used cars will likely see the vehicle driving on the road even longer. The same goes for those buying new ones.

With most automakers now building such durable cars, they compete by adding more high-tech features. Features like adaptive cruise control and Apple CarPlay are now more common than ever on entry-level vehicles. Read on to see our tips on buying a car below.

How to Leverage Incentives to Buy a New Car

In June, car incentives comprised 6.4% of the average deal, or $3,100, down from 6.7% in May. To take advantage of incentives, read about our monthly best car deals to find dealer or manufacturer incentives, including cash back and lower interest rates for financing your next vehicle.

RELATED: How to Buy a New Car in 10 Steps

Selling a Car Right Now

Few of us can sell a car without needing to buy a replacement. But, if that’s you, what are you waiting for? You could get more for your vehicle if it’s in high demand, and that’s excellent news. The best way to get the most money for your used car is to sell it privately. But if you don’t want the hassle, there is still an opportunity to sell to a dealership.

PRO TIP: If selling a car, consider selling it peer-to-peer using Kelley Blue Book’s Private Seller Exchange marketplace. It’s a low-cost method that helps consumers earn more for their vehicle than selling to a dealership.

Trading in a Car Now

The ongoing shortage of used cars will be with us for years. As a result, you’ll likely still see respectable offers for your used car this month.

“Fewer new vehicles produced in 2021 meant lower leasing, which equals fewer lease maturities starting this year,” said Jeremy Robb, senior director of Economic and Industry Insights at Cox Automotive. After being low for the last two years, used-vehicle supply is expected to improve later in 2024 — but that will be without much help from off-lease supply.”

Searching for a decent price for your trade-in is still a good idea by shopping it around. Each dealership tries to keep a balance of vehicles on its lot. Sometimes, the one you want to buy from doesn’t need your trade-in desperately, but a competitor does.

Research your vehicle’s Kelley Blue Book value, then call several local dealerships to see what they’ll offer you for it. Or try our Instant Cash Offer tool, which brings the deal to you from various dealerships without obligation. You can choose your preferred offer or use it to negotiate with others.

Looking Ahead

According to the Cox Automotive/Moody’s Analytics Vehicle Affordability Index, new vehicle affordability improved throughout last year. That trend is continuing so far in 2024.

However, car shoppers can expect the second half of 2024 to look better since any interest rate cut could help affordability. Easing inflation could relieve car buyers if the Federal Reserve lowers rates this year.

RELATED: 10 Best Used Car Deals

Tips for Buying a Vehicle Right Now

If you shop right now, we recommend a few strategies to help you find the right new or used car that fits your budget.

- Expand your search. Widen your search to a broader geographic area.

- Stay patient. Call dealerships early and often to see what’s coming off the trucks for those harder-to-find vehicles. Leave a refundable deposit if you want first dibs.

- Buy a less expensive model. With higher car loan interest rates, consider buying a cheaper vehicle model instead of a more expensive one in the lineup you’re considering.

- Understand the timing. Be prepared to compare deals, and know it involves calling or visiting several dealerships as you look for the right fit.

- Don’t jump. Shop around your trade-in as aggressively as you seek out the right car. Don’t accept the first offer. You could sell yourself short.

- Weigh your options. Don’t just look for a car; search for the best interest rates from banks or credit unions. Also, shop for your insurance rates ahead of the deal to know how much the higher auto insurance costs will cost for your desired vehicle. Then, weigh all your options, including financing incentives and deals at the dealership, if that’s where you buy your next vehicle. Also, you may find the price differences of some newer model used vehicles are almost the same as new cars. Just keep all your options open during your search.

- Don’t pay dealer markups. If you see a markup, sometimes called a market adjustment, on your final invoice, ask that it be removed or shop at another dealership.

- Question all add-ons. If your sales summary includes entries like “window tint” or “fabric protection” and other add-ons you didn’t request, ask for those line items to be removed from your invoice. Many dealers tack on these extras to make quick profits.

It may make sense to keep your existing car for another year. If you must buy, be prepared to take excellent care of your next car to keep it running for a long time.

Related Articles About Car Buying and Selling:

Editor’s Note: This article has been updated since it was initially published.